Each month, we publish a series of articles of interest to homeowners -- money-saving tips, household safety checklists, home improvement advice, real estate insider secrets, etc. Whether you currently are in the market for a new home, or not, we hope that this information is of value to you. Please feel free to pass these articles on to your family and friends.

In This Issue:

-

Essential Tips for Buying in a Competitive Market

Learn how to prepare, move quickly, and make stronger decisions when homes are selling fast.

Read More » -

Appraisal 101: How It Works and How to Prepare

Understand what appraisers look for and why the appraisal can affect the outcome of a sale.

Read More » -

Going Green? What You Need to Know About Energy-Efficient Homes

See how energy efficiency can affect comfort, costs, resale value, and long-term ownership decisions.

Read More »

Essential Tips for Buying in a Competitive Market

Buying a home in a competitive market can feel stressful, especially when good properties attract multiple offers quickly. Buyers may feel pressured to move fast, stretch their budget, or make decisions before they feel fully ready. The key is not to panic. The strongest buyers prepare before the right property appears, understand what matters to sellers, and make offers that are both competitive and responsible. This report explains how buyers can improve their chances without making reckless decisions.

1. Get Fully Prepared Before You Start Touring

In a competitive market, preparation matters more than speed alone. Buyers should have mortgage pre-approval, proof of funds, a clear budget, and a realistic understanding of closing costs before viewing serious properties. If buyers wait until they find a home to organize financing, they may lose valuable time. A prepared buyer can act quickly without feeling rushed because the major financial questions have already been answered.

2. Know Your Maximum Number Before Emotions Take Over

Competition can make buyers feel like they need to keep increasing their offer. Before entering any bidding situation, buyers should decide their true maximum price. This number should reflect not only what the lender may approve, but what the buyer can comfortably afford after accounting for taxes, insurance, utilities, maintenance, and lifestyle needs. Knowing the limit in advance helps prevent emotional overbidding and post-purchase regret.

3. Understand The Local Market Before Making An Offer

A strong offer is based on evidence, not guesswork. Buyers should review recent comparable sales, average days on market, list-to-sale price ratios, and current inventory. Some properties are priced low to attract multiple offers, while others may already be close to market value. Understanding the local pricing strategy helps buyers avoid both underbidding and overpaying.

4. Be Ready To Move Quickly, But Not Carelessly

Competitive markets reward buyers who can act decisively. However, acting quickly does not mean ignoring important details. Buyers should review property disclosures, ask questions, understand included items, and consider potential repair or maintenance concerns. A fast decision should still be an informed decision. Good preparation makes that possible.

5. Make Your Offer Clean And Clear

Sellers often prefer offers that are easy to understand and likely to close. A clean offer may include a strong deposit, clear timelines, flexible closing terms, and only necessary conditions. Buyers should not remove protections without understanding the risk, but they should avoid unnecessary complications that weaken the offer. The goal is to make the seller feel confident that the transaction will proceed smoothly.

6. Look For Terms That Matter Beyond Price

Price is important, but it is not always the only deciding factor. Some sellers may value a flexible closing date, a lease-back option, fewer delays, or confidence in the buyer's financing. A skilled agent can help determine what matters most to the seller. Matching the seller's needs can make an offer more attractive without requiring the buyer to simply pay more.

7. Avoid Chasing Every Property

Not every home is worth competing for. Buyers should be clear about their must-haves, nice-to-haves, and deal-breakers. Chasing every property can lead to fatigue and poor decisions. In a competitive market, discipline is a major advantage. The right goal is not to win any home. The goal is to secure the right home at a price and with terms that still make sense.

8. Stay Patient After Losing An Offer

Losing an offer can be discouraging, especially after investing time and emotion. However, buyers should treat each attempt as market feedback. If offers are consistently too low, the search criteria may need adjustment. If properties are selling beyond the comfort zone, it may be time to consider different neighborhoods, property types, or timing. Staying patient helps buyers avoid making an expensive decision out of frustration.

Conclusion:

Buying in a competitive market requires preparation, discipline, and strategy. The strongest buyers are ready before the right property appears, understand market value, and know their financial limits. A competitive offer should be strong, but it should also be responsible. With the right plan, buyers can compete confidently without sacrificing their long-term financial stability.

Appraisal 101: How It Works and How to Prepare

An appraisal can play an important role in a real estate transaction, especially when financing is involved. Buyers and sellers often focus on the agreed sale price, but a lender may need an independent opinion of value before approving the final mortgage. If the appraisal comes in lower than expected, it can create stress, delays, or renegotiation. This report explains what appraisals are, how they work, and how buyers and sellers can prepare.

1. What An Appraisal Is

An appraisal is an opinion of a property's value prepared by a qualified appraiser. The appraiser reviews the property, compares it to recent sales, and considers market conditions. The purpose is not to confirm what the buyer wants to pay or what the seller hopes to receive. The purpose is to provide an independent estimate of value, often for the lender's risk assessment.

2. Why Lenders Care About Appraisals

When a buyer uses financing, the property often serves as security for the mortgage. The lender wants to know that the property is worth enough to support the loan amount. If the appraisal is lower than the purchase price, the lender may reduce the approved loan amount or request additional information. This can affect the buyer's ability to close unless the issue is resolved.

3. What Appraisers Look At

Appraisers consider location, lot size, property type, square footage, condition, age, updates, layout, features, and recent comparable sales. They also consider market trends and the desirability of the area. Appraisers are not simply looking at decor or personal style. They are evaluating market value based on evidence and property characteristics.

4. Why Comparable Sales Matter

Comparable sales, often called comps, are one of the most important parts of the appraisal process. Appraisers review similar properties that have recently sold nearby. If the subject property is larger, more updated, or in a better location than the comps, adjustments may be made. If it is less desirable or needs work, that may also affect value. Strong comparable sales support a strong appraisal.

5. How Sellers Can Prepare

Sellers can prepare by making the home accessible, clean, and well maintained. They should provide a list of major updates, repairs, permits, upgrades, and improvements. Receipts, renovation details, and maintenance records can help the appraiser understand what has been done. Sellers should not exaggerate, but they should make sure important improvements are easy to identify.

6. How Buyers Can Prepare

Buyers should understand that an appraisal is not guaranteed to match the purchase price. This is especially important in competitive markets where buyers may offer above list price. Buyers should speak with their lender about what happens if the appraisal is low. They should also understand whether they have enough funds to cover a gap if required and whether their offer includes protections related to financing.

7. What Happens If The Appraisal Is Low

A low appraisal does not automatically end the transaction, but it creates a problem that must be solved. The buyer may bring more cash, the seller may reduce the price, the parties may renegotiate, or additional comparable sales may be reviewed. In some cases, a second appraisal may be requested. The available options depend on the agreement, lender requirements, and the willingness of both parties to work toward a solution.

8. Why Pricing Correctly Matters

For sellers, realistic pricing helps reduce appraisal risk. A property priced far above market value may attract attention but can create problems when financing is involved. A strong pricing strategy uses recent sales, current competition, property condition, and buyer demand. The goal is not only to attract offers, but to support a transaction that can close.

Conclusion:

An appraisal is an important checkpoint in many real estate transactions. It protects lenders, informs buyers, and can influence whether a sale moves forward smoothly. Sellers can prepare by documenting improvements and pricing realistically. Buyers can prepare by understanding lender requirements and planning for possible value gaps. The best transactions are supported by strong pricing, clear evidence, and realistic expectations.

Going Green? What You Need to Know About Energy-Efficient Homes

Energy-efficient homes are becoming more important to buyers, sellers, and homeowners. Rising utility costs, environmental awareness, and comfort concerns all contribute to growing interest in greener properties. However, not every upgrade provides the same value, and not every energy-efficient feature is easy to evaluate at first glance. This report explains what buyers and sellers should know about energy-efficient homes, how improvements can affect ownership costs, and which features may matter most.

1. Understand What Energy Efficiency Really Means

An energy-efficient home uses less energy to provide the same or better comfort. This can involve insulation, windows, heating and cooling systems, appliances, lighting, ventilation, water heating, and smart controls. A truly efficient home is not defined by one feature. It is the result of several systems working together to reduce waste and improve performance.

2. Look Beyond The Marketing Language

Terms like "green," "eco-friendly," and "energy-saving" can sound impressive, but buyers should look for details. What upgrades were completed? When were they done? Were permits required? Are there receipts, warranties, or energy reports? Clear documentation is more valuable than vague claims. Sellers should be prepared to show evidence of improvements rather than relying only on general descriptions.

3. Insulation And Air Sealing Matter

Some of the most valuable energy improvements are not always visible. Proper insulation and air sealing can reduce heat loss, improve comfort, and lower energy bills. Drafty homes can feel uncomfortable even with newer heating or cooling systems. Buyers should pay attention to attic insulation, basement insulation, window seals, door weatherstripping, and signs of drafts or uneven temperatures.

4. Heating And Cooling Systems Affect Long-Term Costs

Heating and cooling often represent a major share of household energy use. Efficient furnaces, heat pumps, air conditioners, boilers, and ventilation systems can reduce monthly costs and improve comfort. However, age, maintenance, sizing, and installation quality matter. A high-efficiency system that has been poorly maintained may not perform as expected. Buyers should review service records where available.

5. Windows And Doors Can Help, But Cost Matters

Newer windows and doors can improve comfort, reduce drafts, and enhance appearance. However, replacement can be expensive. Buyers should evaluate both condition and performance. Sellers should understand that window upgrades may help marketability, but they may not always return every dollar spent. The best improvements are usually those that solve obvious comfort or efficiency problems.

6. Appliances And Lighting Are Easy Wins

Energy-efficient appliances, LED lighting, smart thermostats, and water-saving fixtures are easier upgrades that can appeal to buyers. These improvements may not transform the property's value on their own, but they contribute to a modern and well-maintained impression. For sellers, small efficiency upgrades can support the overall presentation of the home.

7. Consider Solar And Renewable Features Carefully

Solar panels and renewable energy systems can be attractive, but buyers need to understand ownership, contracts, warranties, maintenance, and transfer requirements. A system that is owned outright may be different from one that is leased or financed. Buyers should review all documentation before assuming the feature adds value. Sellers should have the paperwork ready before listing.

8. Energy Efficiency Can Support Resale Value

Many buyers appreciate lower operating costs and improved comfort. Energy-efficient features can make a home stand out, especially when supported by documentation. However, value depends on the market, the quality of the improvements, and buyer awareness. A home that is efficient, comfortable, well maintained, and easy to understand is more likely to appeal to practical buyers.

Conclusion:

Energy-efficient homes can offer lower costs, better comfort, and stronger long-term appeal. Buyers should look past marketing language and evaluate the actual systems, documentation, and performance of the property. Sellers should highlight genuine improvements clearly and provide supporting records. Going green is not just about one upgrade. It is about creating a home that performs better, costs less to operate, and feels better to live in.

Winter Haven, FL Home For Sale

|

Get a Cash Offer in 48 Hours — Sell Your Central Florida Home Fast! Get a Cash Offer in 48 Hours — Sell Your Central Florida Home Fast!

|

Attention Central Florida Home Buyers!Attention Central Florida Home Buyers! Come and see this Awesome home owned by an Executive Chef with Disney. This home comes equipped with a back yard with many of the fresh Fruits, Vegetables, and Spices to Cook like an experienced Chef to feed your family and keep them healthy. This Open Floor plan home is laid out perfectly for a family to enjoy their time together.

|

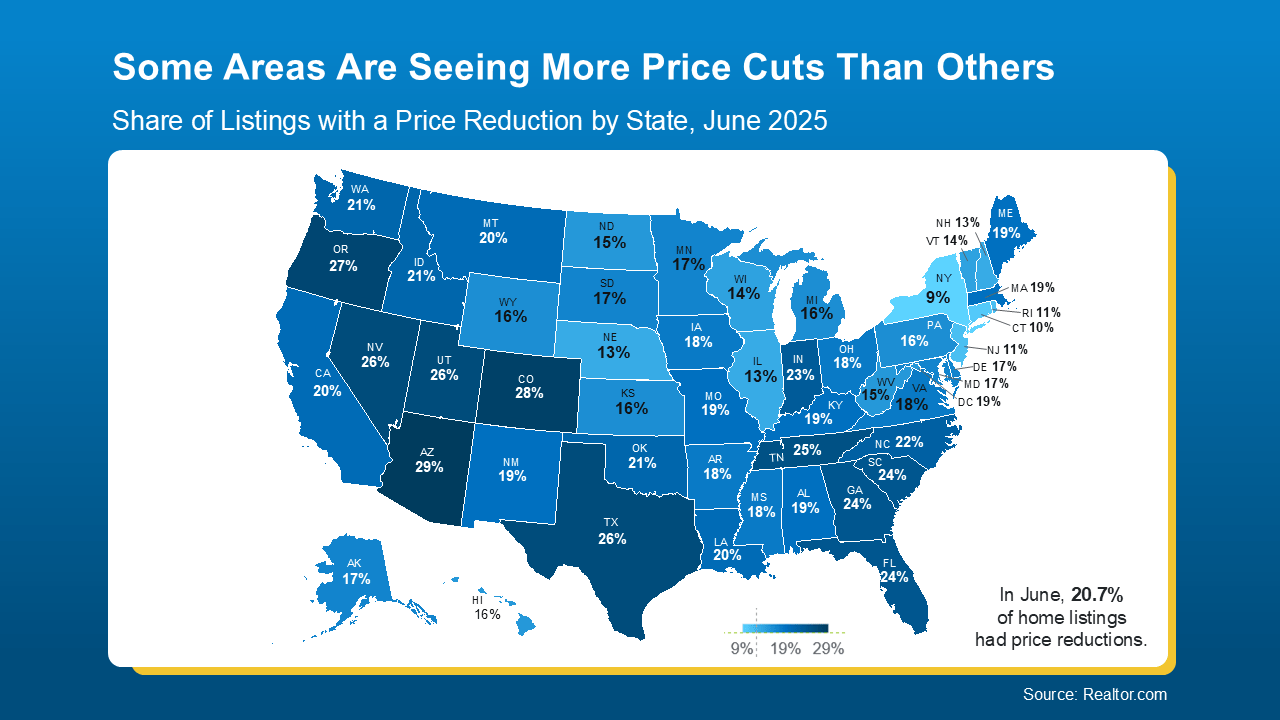

The 3 Things You Risk by Pricing Too HighWhen selling your house, the price you choose isn’t just a number, it's a strategy. And in today’s market, that strategy needs to be sharp. The number of homes for sale is climbing. And that means buyers have more choices and can be more selective. If your price doesn’t line up with what else is out there, they’ll scroll right past it and go on to the next one. Pricing right from the start is your best move – and a great agent can help make sure you do. And more sellers are finding that out the hard way. They list their house based on how things were a year ago – or based on a neighbor’s sale that happened under completely different circumstances. Then, when their house doesn’t sell, they’re left with three tough choices: None of those options were part of the original plan. And honestly, none of them are where you should end up if you wanted to sell. Here’s a look at how a local agent’s expertise can help you avoid these headaches. Let's use price cuts as an example. While the number of price cuts is up nationally, data shows some parts of the country are seeing far more of them than others. It all comes down to how much inventory has grown in that area (see map below): That means pricing isn’t one-size-fits-all. What’s happening nationally might not reflect what’s happening in your zip code, and that’s why you shouldn’t try to determine your list price on your own. A skilled agent doesn’t just toss out a number. As Zillow says: And that’s all knowledge your agent will have. They study your local market, compare recent sales, and factor in your goals and buyer behavior. Based on what’s happening where you live, sometimes the best play will be pricing right at current market value. Other times pricing a little lower actually will spark more offers and ultimately get you a better final sale price. So don’t skimp on the strategy or on your agent. With their local market know-how, you’ll be able to sell quickly, even in a shifting market. Overpricing can lead to tough choices you never want to face. But with the right price, and the right guidance, you can skip the stress and sell with confidence. Let’s connect so you have a pricing strategy that works for today’s market and gets you where you want to go.

|

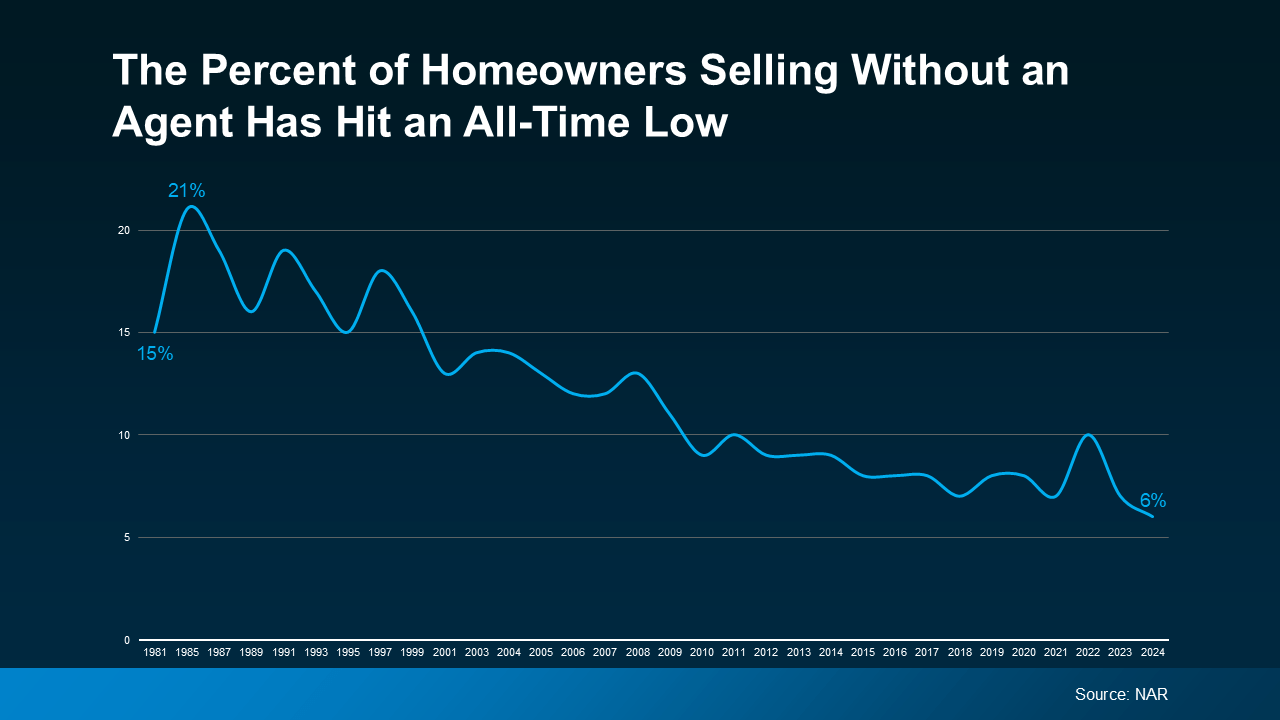

Why Most Sellers Hire Real Estate Agents TodaySelling your house without an agent as a “For Sale by Owner” (FSBO) may be something you’ve considered. But you should know that, in today’s shifting market, more homeowners are deciding that’s just not worth the risk. According to the latest data from the National Association of Realtors (NAR), the number of homeowners selling without an agent has hit an all-time low (see graph below): A recent survey finds three out of every four homeowners who don’t plan to use an agent have doubts about whether that’s actually the right decision. And here’s why. The market is changing – not in a bad way, just in a way that requires a smarter, more strategic approach. And having a real estate expert in your corner really pays off. Here are just two of the ways an agent's expertise makes a difference. One of the biggest hurdles when selling a house on your own is figuring out the right price. It’s not as simple as picking a number that sounds good or selling your house for what your neighbor’s sold for a few years back – you need to hit the bullseye for where the market is right now. Without an agent’s help, you’re more likely to miss the mark. As Zillow explains: Basically, they know what’s really selling, what buyers are willing to pay in your area, and how to position your house to sell quickly. That kind of insight can have a big impact, especially in a market that’s balancing out. There’s also a mountain of documentation when selling a house, including everything from disclosures to contracts. And a mistake can have big legal implications. This is another area where having an agent can help. They’ve handled these documents countless times and know exactly what’s needed to keep everything on track, so you avoid delays. And now that buyers are including more contingencies again and asking for concessions, your agent will guide you through each form step by step, making sure it’s done right and documented correctly the first time. Now that the number of homes for sale has grown, homes aren’t selling at quite the same pace they were. But you can still sell quickly if you have a proven plan to help your house stand out. Just remember, homeowners don’t have the same network or marketing tools an experienced agent does. So, if you want the process to happen fast, you’ll likely want a pro by your side. Having the right agent and the right strategy is key in a shifting market. Let’s connect so you don’t have to take this on solo – and so you can list with confidence, knowing you’ve got expert guidance from day one.

|

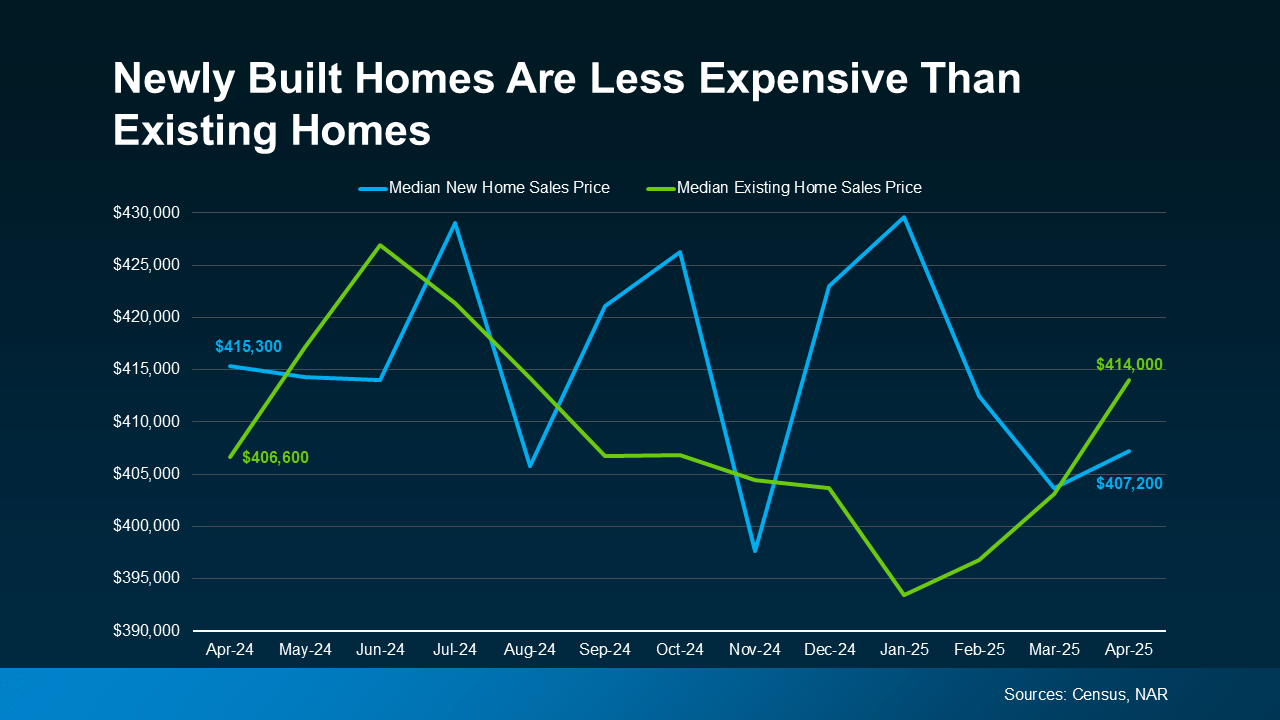

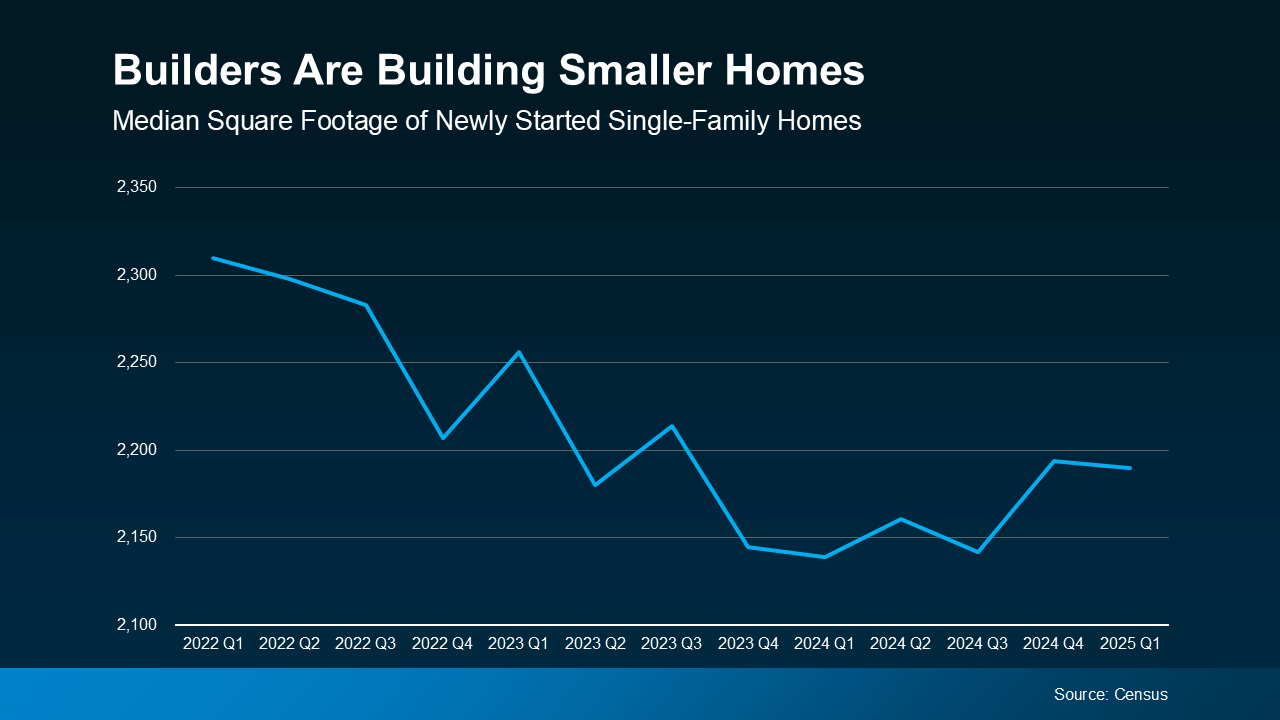

Newly Built Homes May Be Less Expensive Than You ThinkDo you think a brand-new home means a bigger price tag? Think again. Right now, something unique is happening in the housing market. According to the Census and the National Association of Realtors (NAR), the median price of newly built homes is actually lower than the median price for existing homes (ones that have already been lived in): 1. Builders Are Building Smaller Homes Builders know that buyers are struggling with affordability today. So, instead of building big houses that may not sell, they’re building smaller ones that will. According to the Census, the average size of a newly built single-family home has dropped considerably over the past few years (see graph below): 2. Builders Are Offering Price Cuts and Incentives In May, according to the National Association of Home Builders (NAHB), 34% of builders lowered their prices, with an average price drop of 5%. That’s because they want to be sure they’re selling the inventory they have before they build more. On top of that, 61% of builders also offered sales incentives – like helping with closing costs or buying down your mortgage rate. These are all ways builders are making their homes more affordable, so these homes sell in today’s market. If you're trying to buy a home right now, be sure to talk to your agent to find out what builders are doing in and around your area. They can find new home communities, as well as builders who are offering incentives or discounts, and hidden gems you might not uncover on your own. Plus, buying a newly built home often means there are different steps in the process than if you purchase a home that’s been lived in before. That’s why it’s so important to have your own agent who can explain the fine print. You want a pro in your corner to advocate for you, negotiate on your behalf, and make sure your best interests come first. You could get a home that’s brand new, with modern features, at a price that’s even lower than some older homes. Let’s talk about what you’re looking for and see if a newly built home is the right fit for you. If buying a home is on your to-do list, what would stop you from exploring newly built options?

|

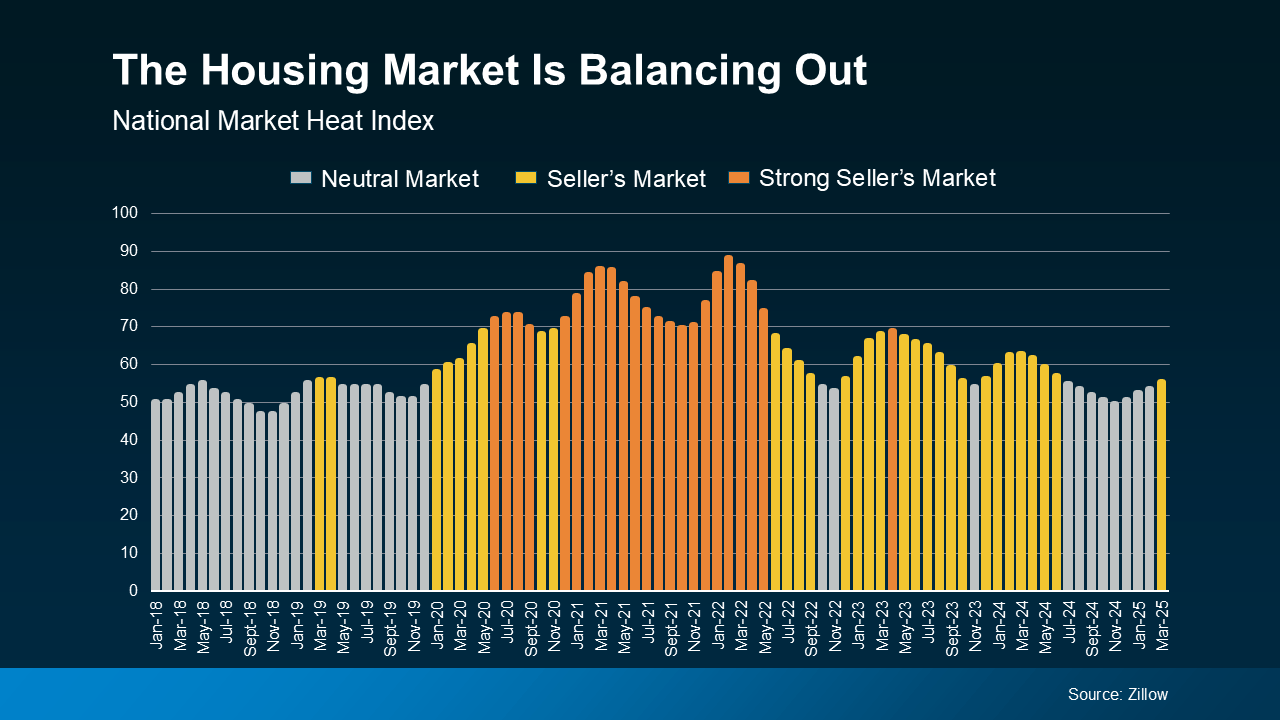

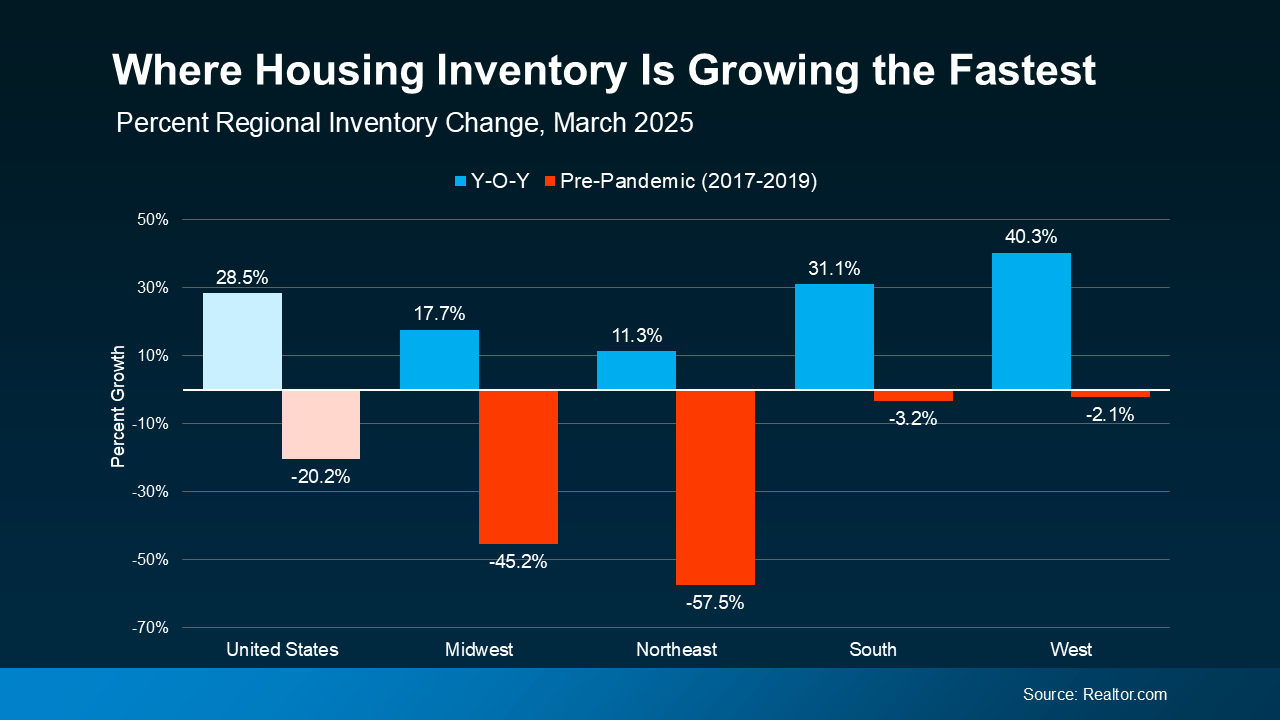

A Tale of Two Housing MarketsFor a long time, the housing market was all sunshine for sellers. Homes were flying off the shelves, and buyers had to compete like crazy. But lately, things are starting to shift. Some areas are still super competitive for buyers, while others are seeing more homes sit on the market, giving buyers a bit more breathing room. In other words, it’s a tale of two markets, and knowing which one you’re in makes a huge difference when you move. In a buyer’s market, there are a lot of homes for sale, and not as many people buying. With fewer buyers competing for these homes, that means they generally sit on the market longer, they might not sell for as much as they would in a seller’s market, and buyers have more room to negotiate. On the flip side, in a seller’s market, there aren’t enough homes for sale for the number of buyers who are trying to purchase them. Homes sell faster, sellers often get multiple offers, and prices shoot higher because buyers are willing to pay more to win the home. For years, almost every market in the country was a strong seller’s market. That made it tough for buyers – especially first-timers. But now, things are shifting. According to Zillow, the national housing market is balancing out (see graph below): The orange bars in the middle of the graph show the years when sellers had their strongest advantage, from 2020 to early 2022. But, as time has gone on, the market has become more balanced. It shifted from a strong seller’s market to a less intense one. And lately, it's been neutral more than anything else (that’s the gray bars on the right side of the graph). That means buyers are gaining some negotiating power again. In a more balanced or neutral market, homes tend to stay on the market a little longer, bidding wars are less common, and sellers may need to make more concessions – like price reductions or helping with closing costs. That shift gives today’s buyers more opportunities and less competition than a couple of years ago. Inventory plays a big role. When there are more homes for sale, buyers have more options – and that cools down home price growth. As data from Realtor.com shows, the supply of available homes for sale isn’t growing at the same rate everywhere (see graph below): The South and West regions of the U.S. have seen big jumps in housing inventory in the past year (that’s the blue on the right). Both are almost back to pre-pandemic levels. That’s why more buyer’s markets are popping up there. But in the Northeast and Midwest, inventory is still very low compared to pre-pandemic (that’s why those red bars are so big). That means those areas are more likely to stay seller’s markets for now. Every local market is different. Even if the national headlines say one thing, your town (or even your neighborhood) could be telling a totally different story. Knowing which type of market you’re in helps you make smarter decisions for your move. That’s why working with a local real estate agent is so important right now. As Zillow says: Agents understand the unique trends in your area and can help you make the best choices, whether you’re buying or selling. With their expert strategies, you can move no matter which way the market is leaning, because they know how to navigate various levels of buyer competition, how to find hidden gems locally, how to price a house right, how to negotiate based on who has more leverage, and more. If you're ready to make a move, or even just thinking about it, let’s connect. That way, you’ll have someone to help you understand our local market and create a game plan that works for you. What’s one thing you’re curious about when it comes to the market in our area?

|

The Spring Guides for Buying or Selling a Home Are HereThe Spring Guides for buying or selling a home are here. Let’s connect so you can get the latest digital copies of these guides.

|